You stepped into what should have been a routine rideshare trip, and now you are dealing with injuries, mounting medical bills, and a shocking piece of news: the Uber or Lyft driver’s personal insurance has denied your claim. This situation is far more common than most people realize, and it leaves accident victims feeling powerless and confused. If you are asking yourself, “What if the Uber or Lyft driver’s personal insurance denies my claim?” — you are not alone, and you are not out of options.

At Pencheff & Fraley, our experienced rideshare accident attorneys have helped injured clients across Florida navigate the complex, multi-layered world of rideshare insurance. A denial from the driver’s personal insurer is not the end of the road. Understanding why these denials happen, which other policies may apply, and what legal remedies are available to you is the first step toward recovering the compensation you deserve.

Why Would a Rideshare Driver’s Personal Insurance Deny Your Claim?

When you file a claim against an Uber or Lyft driver’s personal auto insurance after an accident, you may be surprised to receive a denial letter. Insurance companies are not simply being difficult — in many cases, they have a contractual basis for refusing to pay. There are two primary reasons this happens.

The “Commercial Use” Exclusion: A Critical Policy Gap

Nearly every standard personal auto insurance policy contains a “commercial use” or “livery” exclusion. This clause specifically states that the policy will not cover losses that occur while the insured vehicle is being used for commercial purposes — and transporting passengers for a fee through a rideshare platform is unambiguously a commercial activity.

When a driver signs up with Uber or Lyft, they are essentially operating a small transportation business using their personal vehicle. Their personal insurer, however, wrote the policy assuming the car would be used for personal errands, commuting, and leisure — not for commercial hire. The moment the driver activates the rideshare app, the personal policy’s coverage becomes legally questionable, and the moment an accident occurs, the insurer will almost certainly invoke this exclusion to deny the claim.

Material Misrepresentation: When the Driver Wasn’t Honest

A second basis for denial is material misrepresentation. If the driver failed to disclose to their personal insurer that they were using their vehicle for rideshare activities, the insurer can argue that the policy was issued based on false or incomplete information. In Florida and most other states, insurers have the right to rescind a policy or deny a claim when the insured made a material misrepresentation at the time of application.

This scenario is particularly problematic for accident victims because it can leave them in a situation where neither the driver’s personal insurer nor the rideshare company’s insurer initially steps forward to pay. However, as our attorneys at Pencheff & Fraley can attest, this does not mean compensation is unavailable — it simply means you need to know where to look next.

Understanding Uber and Lyft’s Insurance Coverage Periods

The most important concept to understand after a rideshare accident is that coverage depends entirely on what the driver was doing at the exact moment of the crash. Both Uber and Lyft structure their insurance around three distinct “periods” of driver activity, and the applicable coverage — and its limits — changes dramatically from one period to the next.

| Coverage Period | Driver Status | Coverage Available |

| Period 0 (App Off) | App not active; personal use | Driver’s personal auto insurance only |

| Period 1 (App On, No Ride) | Logged in, waiting for a request | Contingent liability: $50K/person, $100K/accident, $25K property damage |

| Period 2 & 3 (Ride Accepted / Passenger On Board) | En route to pickup or actively transporting a passenger | Up to $1 million third-party liability; UM/UIM coverage; contingent collision/comprehensive |

Sources: Uber’s Official Insurance Page; Lyft’s Insurance Resources

Period 0: App Off — Personal Insurance Is the Only Option

When the driver’s app is completely off, they are simply a private citizen driving their own car. The rideshare company has no involvement, and the driver’s personal auto insurance is the sole applicable policy. If that policy denies the claim based on a commercial use exclusion, and the driver was truly offline, you may need to explore other avenues such as your own uninsured/underinsured motorist (UM/UIM) coverage.

Period 1: App On, Waiting for a Request — Contingent Coverage Kicks In

This is the most legally complex and frequently disputed period. The driver is logged into the app and available for rides but has not yet accepted a specific request. During Period 1, Uber and Lyft provide contingent liability coverage — but critically, this coverage is secondary. It is specifically designed to apply when the driver’s personal insurance denies the claim or is insufficient to cover the damages.

According to Uber’s official insurance documentation, Period 1 coverage provides at least $50,000 per person in bodily injury liability, $100,000 per accident in total bodily injury liability, and $25,000 in property damage liability. These limits are significantly lower than what is available in Period 3, which is why establishing the driver’s exact app status at the time of the crash is so critical.

Period 2 & 3: Ride Accepted or Passenger On Board — Maximum Coverage

Once the driver accepts a ride request and is actively en route to pick up a passenger (Period 2) or has a passenger in the vehicle (Period 3), the rideshare company’s full commercial insurance policy activates. This policy provides up to $1 million in third-party liability coverage, along with uninsured/underinsured motorist protection and, in some cases, contingent collision and comprehensive coverage.

For passengers injured during an active ride, this $1 million policy is the primary source of compensation. For third parties — such as pedestrians, cyclists, or occupants of other vehicles — this policy also provides robust protection. As we discuss in our detailed guide on Florida Uber & Lyft accident laws, Florida Statute § 627.748 mandates these coverage minimums for all Transportation Network Companies (TNCs) operating in the state.

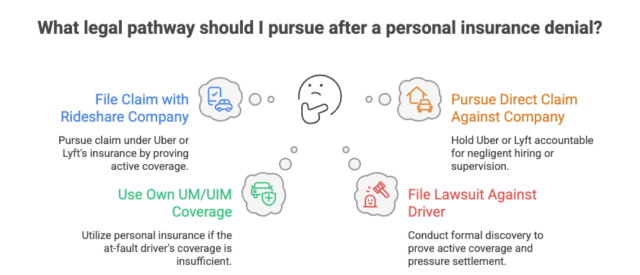

What Are Your Options After a Personal Insurance Denial?

A denial from the driver’s personal insurer is not the final word. There are several legal pathways available to you, and an experienced rideshare accident attorney can help you identify which ones apply to your specific situation.

Option 1: File a Claim Directly with Uber or Lyft’s Insurance

If the driver’s personal insurance denies your claim, the next logical step is to pursue a claim under the rideshare company’s own commercial insurance policy. Both Uber and Lyft maintain substantial insurance programs, but accessing these policies requires proving that the driver was in an active coverage period at the time of the accident.

This is where things can get contentious. Rideshare companies and their insurers will scrutinize the driver’s app data to determine their exact status. They may argue that the driver was in Period 0 (app off) rather than Period 1 or 2, which would eliminate their coverage obligation. An attorney can subpoena the platform’s server logs, GPS data, and dispatch records to challenge these claims and establish the true status of the driver’s app at the time of the crash.

Option 2: Utilize Your Own Uninsured/Underinsured Motorist (UM/UIM) Coverage

If you carry uninsured/underinsured motorist (UM/UIM) coverage on your own personal auto insurance policy, you may be able to file a claim under that policy when the at-fault driver’s coverage is insufficient or has been denied. UM/UIM coverage is specifically designed to protect you in situations where the responsible party cannot or will not pay.

In Florida, UM/UIM coverage is not mandatory, but it is strongly recommended — particularly given the prevalence of rideshare vehicles on Florida roads. If you have this coverage, your own insurer steps into the shoes of the uninsured or underinsured driver and compensates you for your injuries and damages. Your insurer may then pursue subrogation against the at-fault driver or the rideshare company’s insurer to recover what it paid you.

Option 3: File a Lawsuit Against the At-Fault Driver

Filing a personal injury lawsuit against the rideshare driver is another viable option. A lawsuit allows your attorney to conduct formal discovery, which includes demanding the driver’s app data, insurance application documents, and any communications with the rideshare company. This evidence is often crucial to proving that the driver was in an active coverage period and that the rideshare company’s insurance should apply.

Additionally, a lawsuit puts significant pressure on the driver and their insurer to settle, as the costs and risks of litigation often motivate parties to negotiate in good faith. Our attorneys at Pencheff & Fraley have extensive experience litigating rideshare accident cases and know how to build the strongest possible case on your behalf.

Option 4: Pursue a Direct Claim Against Uber or Lyft

While Uber and Lyft classify their drivers as independent contractors — a legal shield designed to limit their direct liability — there are circumstances under which the companies themselves can be held accountable. As we explain in our article on whether Uber passengers can sue after an accident, claims of negligent hiring, negligent retention, or negligent supervision can pierce the independent contractor defense.

For example, if Uber or Lyft failed to conduct an adequate background check and allowed a driver with a history of reckless driving onto the platform, the company may bear direct liability for the resulting harm. Similarly, if the company’s app design encourages distracted driving by requiring frequent interaction with the screen while the vehicle is in motion, that could constitute corporate negligence.

Evidence That Can Make or Break Your Rideshare Claim

The outcome of a rideshare accident claim often hinges on the quality of the evidence gathered in the immediate aftermath of the crash. The following types of evidence are particularly important in cases where the driver’s personal insurance has denied the claim.

App Metadata and Server Logs: The rideshare platform maintains detailed records of every driver’s activity, including login times, ride requests, GPS traces, and trip completion data. This information is the single most important piece of evidence for establishing the driver’s coverage period. If the rideshare company refuses to produce these records voluntarily, a court subpoena during litigation can compel their disclosure.

Cell Phone Records and GPS Data: The driver’s cell phone records and GPS data can corroborate or contradict the platform’s records, providing an independent source of evidence about the driver’s location and app status at the time of the accident.

Dashcam and Surveillance Footage: Video footage from dashcams, traffic cameras, or nearby businesses can provide objective evidence of how the accident occurred, the driver’s behavior leading up to the crash, and the severity of the impact.

Witness Statements: Passengers, other drivers, and bystanders who witnessed the accident can provide valuable testimony about the circumstances of the crash and the driver’s conduct.

Insurance Application Documents: In cases involving material misrepresentation, the driver’s insurance application and renewal documents can reveal what the driver told their insurer about the vehicle’s use, which is critical to challenging or supporting a denial.

How a Rideshare Accident Lawyer Can Help You

The legal landscape surrounding rideshare accidents is genuinely complex. Multiple insurance policies, shifting coverage periods, corporate liability shields, and aggressive insurance defense teams all work against injured victims. Having an experienced rideshare accident attorney in your corner can make a decisive difference in the outcome of your case.

Investigating the Accident and Establishing Liability

Our attorneys conduct thorough, independent investigations into every rideshare accident we handle. We work with accident reconstruction experts, obtain and analyze the driver’s app data, review police reports, and interview witnesses to build a complete picture of what happened and who is responsible.

Navigating the Multi-Layer Insurance System

As detailed in our guide on sorting through rideshare insurance coverage complications, rideshare accidents can involve the driver’s personal policy, the rideshare company’s commercial policy, your own UM/UIM coverage, and potentially other third-party policies — all at the same time. We know how to identify which policies apply, in what order, and how to maximize the total compensation available to you.

Negotiating Aggressively on Your Behalf

Insurance companies have entire teams of adjusters and defense attorneys whose job is to minimize payouts. Our attorneys have the experience and tenacity to negotiate aggressively on your behalf, countering lowball offers and pushing back against improper denials. We do not settle for less than what our clients deserve.

Litigating Your Case if Necessary

If a fair settlement cannot be reached through negotiation, we are fully prepared to take your case to trial. Our firm has a proven track record of success in personal injury litigation, and insurance companies know we are willing to fight for our clients in court.

Frequently Asked Questions About Rideshare Insurance Denials

Q: If the driver’s personal insurance denies my claim, does Uber or Lyft automatically pay?

A: Not automatically. The rideshare company’s coverage applies only during specific periods and under their policy’s terms. Whether Uber or Lyft pays depends on whether the driver was in a covered period — logged in, en route to a pickup, or actively transporting a passenger — at the time of the accident. An attorney can help you gather the evidence needed to establish this.

Q: Can I sue Uber or Lyft directly for my injuries?

A: It is possible, but challenging. Uber and Lyft classify their drivers as independent contractors to limit direct liability. However, you may have a direct claim against the company if they were negligent in hiring, retaining, or supervising the driver. Our attorneys can evaluate whether a direct claim against the rideshare company is viable in your case.

Q: What if the rideshare company claims the driver’s app was off at the time of the accident?

A: Do not accept this at face value. Rideshare companies have a financial incentive to argue that the driver was offline, as this eliminates their coverage obligation. Your attorney can subpoena the platform’s server logs and the driver’s GPS data to independently verify the driver’s app status. These records often tell a different story than what the company initially claims.

Q: How long do I have to file a rideshare accident claim in Florida?

A: In Florida, the statute of limitations for personal injury claims is generally two years from the date of the accident, following the 2023 tort reform changes. Missing this deadline can permanently bar you from recovering compensation. It is critical to consult with an attorney as soon as possible after your accident to preserve your rights.

Q: What damages can I recover in a rideshare accident claim?

A: You may be entitled to recover a wide range of damages, including medical expenses (past and future), lost wages and diminished earning capacity, pain and suffering, emotional distress, and property damage. An attorney can assess the full extent of your damages and fight to ensure you receive maximum compensation.

Q: What should I do immediately after a rideshare accident?

A: Your first priority is your health — seek medical attention immediately, even if your injuries seem minor. Then, report the accident through the rideshare app, file a police report, document the scene with photos and videos, collect witness information, and save all trip details from the app. Avoid giving recorded statements to any insurance company before consulting with an attorney. For a detailed step-by-step guide, see our article on what to do if you’re injured as an Uber or Lyft passenger in Florida.

Don’t Let a Denied Claim Stand Between You and the Compensation You Deserve

A denial from the Uber or Lyft driver’s personal insurance is a frustrating setback, but it is not the end of your case. The rideshare insurance system is deliberately complex, and insurance companies count on injured victims not understanding their full range of options. At Pencheff & Fraley, we level the playing field.

Our attorneys have deep experience handling rideshare accident claims across Florida. We understand the tactics insurance companies use to minimize or deny claims, and we know how to counter them effectively. Whether your case involves a Period 1 coverage dispute, a negligent hiring claim against Uber or Lyft, or a UM/UIM claim under your own policy, we have the knowledge and resources to pursue every available avenue of compensation on your behalf.

Contact us today for a free, no-obligation consultation. We will review your case, answer your questions, and explain your legal options. Learn how we can help you on the road to recovery. Pay nothing unless we win your case.

Call us at 904-770-4953 or visit our website at www.pencheffandfraley.com to schedule your free case consultation.

We’re Here for You 24/7

We are available 24/7 to take your call. If you are unable to travel, we will come to you. The sooner you call, the stronger your case can be. Your path to maximum compensation and justice starts with a single phone call to Pencheff & Fraley.

Author: Pencheff and Fraley Legal Team

Disclaimer: This article is for informational purposes only and does not constitute legal advice. Every case is unique, and you should consult with a qualified attorney about your specific situation.