After the shock of a rideshare crash, one question rises above all others: “Will Uber or Lyft insurance pay my medical bills after a crash?” The answer is not a simple yes or no. It depends on what the driver was doing at the moment of impact, who caused the collision, and how quickly you take the right steps to protect your claim. At Pencheff & Fraley, we have helped injured passengers navigate these exact questions — and we want you to have the information you need before the insurance companies start calling.

Rideshare accidents are among the most legally complex personal injury cases because they involve multiple overlapping insurance policies, corporate liability shields, and strict timelines. According to research published by the CDC and the University of Chicago, the widespread adoption of rideshare services has been linked to approximately 987 additional traffic fatalities per year in the United States. A separate University of Illinois Chicago study found that one in three rideshare drivers has been involved in a crash while working. Understanding how Uber and Lyft’s insurance systems work is not just useful — it can be the difference between full compensation and being left with unpaid bills.

How Rideshare Insurance Actually Works: The Three Periods

Both Uber and Lyft structure their insurance coverage around three distinct operational periods that correspond to what the driver is doing at any given moment. This tiered system is the single most important factor in determining whether — and how much — the rideshare company’s insurance will cover your medical bills.

Period 0: The App Is Off

When a driver’s rideshare app is completely off, they are considered a private citizen operating their personal vehicle. In this situation, Uber and Lyft provide zero coverage. Your only recourse is against the driver’s personal auto insurance policy. This matters because many personal auto policies contain exclusions for commercial use, meaning the driver’s insurer may deny the claim if they discover the driver was heading to or from a rideshare zone. This is sometimes called the “coverage gap,” and it leaves many accident victims in a difficult position.

Period 1: App Is On, No Ride Accepted

This is the most misunderstood phase of rideshare insurance. When a driver is logged into the app and available to accept rides — but has not yet accepted a specific trip — both Uber and Lyft provide limited contingent liability coverage. According to Uber’s official insurance page and Lyft’s driver insurance resources, the coverage limits during Period 1 are:

- $50,000 per person for bodily injury

- $100,000 per accident for bodily injury

- $25,000 per accident for property damage

The word “contingent” is critical here. This coverage only activates after the driver’s personal auto insurance has been exhausted or formally denied the claim. This two-step process can delay your compensation by weeks or months while insurers argue over who pays first.

Periods 2 and 3: Ride Accepted Through Drop-Off

This is where the most robust protection exists. From the moment a driver accepts a ride request (Period 2) through the completion of the trip (Period 3), both Uber and Lyft activate their full commercial insurance policy. This includes:

- $1,000,000 in third-party liability coverage — covering passengers, other drivers, pedestrians, and cyclists

- $1,000,000 in uninsured/underinsured motorist (UM/UIM) coverage — protecting you if the at-fault driver has no insurance or insufficient coverage

- Contingent collision and comprehensive coverage for the driver’s vehicle

As a passenger in an Uber or Lyft, you are almost always in Period 2 or 3 — meaning the full $1 million policy applies to your injuries. This is significant protection, but as we explain below, accessing it is rarely straightforward.

| Driver Status | Uber/Lyft Liability Coverage | UM/UIM Coverage | Notes |

| App Off (Period 0) | None | None | Driver’s personal policy only |

| App On, No Ride (Period 1) | $50K per person / $100K per accident / $25K property damage | Varies by state | Contingent on personal policy denial first |

| Ride Accepted or In Progress (Periods 2 & 3) | $1,000,000 | $1,000,000 | Full commercial policy applies |

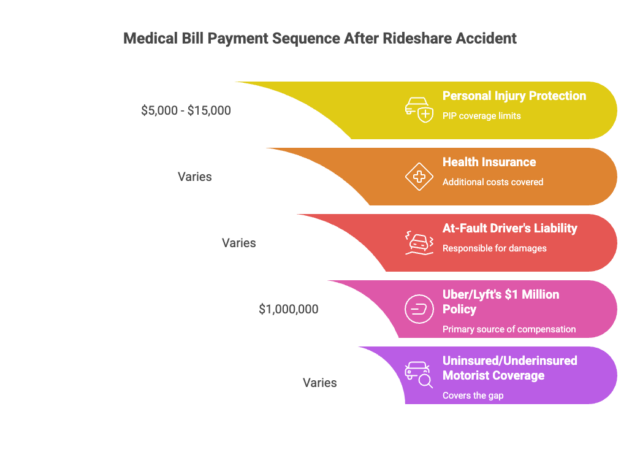

Who Actually Pays Your Medical Bills? A Realistic Look

Knowing the policy limits is one thing. Understanding the real-world sequence of who pays what — and when — is another. Here is how medical bill payment typically unfolds after a rideshare accident.

Step 1: Your Own Personal Injury Protection (PIP) or Health Insurance

In states that require Personal Injury Protection (PIP) insurance — sometimes called “no-fault” coverage — your own auto insurance is typically the first source of payment for your medical bills, regardless of who caused the accident. PIP pays quickly and without requiring you to prove fault, which is valuable when you need immediate treatment.

The challenge is that PIP coverage limits are often low. Many states require only $5,000 to $15,000 in PIP coverage, which can be exhausted by a single emergency room visit and a few follow-up appointments. Once your PIP is depleted, your personal health insurance may cover additional costs, though you will likely face deductibles and co-pays.

Step 2: The At-Fault Driver’s Liability Insurance

If another driver caused the accident — for example, a third party ran a red light and struck the Uber vehicle you were riding in — that driver’s liability insurance is responsible for your damages. This is called a “third-party claim.” If the at-fault driver is uninsured or carries only minimum coverage, this may not be enough to cover serious injuries.

Step 3: Uber or Lyft’s $1 Million Policy

If you were a passenger during an active trip and the Uber or Lyft driver was at fault, or if the at-fault third party is uninsured, the rideshare company’s $1 million policy becomes the primary source of compensation. This policy covers medical expenses, lost wages, pain and suffering, and other damages. However, the rideshare company’s insurer will not simply write you a check. They will investigate the claim, assess liability, and often attempt to minimize the payout.

Step 4: Uninsured/Underinsured Motorist Coverage

If the at-fault driver has no insurance or insufficient coverage, and you were on an active rideshare trip, Uber and Lyft’s UM/UIM coverage can step in to cover the gap. This is one of the most important — and most overlooked — protections available to rideshare passengers. According to Allstate’s rideshare insurance resource, many victims are unaware that this layer of protection even exists, and they settle for far less than they deserve.

Why Getting Paid Is Harder Than It Looks

On paper, the coverage structure seems generous. In practice, rideshare accident claims are routinely delayed, disputed, and denied. Here are the most common obstacles victims face.

Disputes Over the Driver’s App Status

The entire insurance framework hinges on what the driver was doing at the moment of impact. Uber and Lyft track this data through their apps, and their insurers use it aggressively to limit payouts. If there is any ambiguity — for example, if the driver had just ended a trip or was about to accept a new one — the company may argue that only the lower Period 1 limits apply, or that no rideshare coverage applies at all. Resolving these disputes often requires subpoenaing digital records from the rideshare platform, which is a task best handled by an experienced attorney.

The Independent Contractor Defense

Both Uber and Lyft classify their drivers as independent contractors, not employees. This classification is central to their business model and their legal defense strategy. Under the legal doctrine of respondeat superior, employers are liable for the negligent acts of their employees. Because drivers are classified as contractors, Uber and Lyft argue they cannot be held directly liable for a driver’s negligence. This does not mean you have no recourse — but it does mean that holding the company itself accountable requires a more sophisticated legal strategy.

Insurers Pointing Fingers at Each Other

When multiple insurance policies are potentially involved — the driver’s personal policy, the rideshare company’s policy, and your own PIP or health insurance — each insurer has a financial incentive to argue that another policy should pay first. This back-and-forth can leave your medical bills unpaid for months while you wait for the insurers to sort out their responsibilities. As one analysis of the three-period system notes, these coverage gaps are a known and persistent problem in rideshare accident claims.

Lowball Settlement Offers

Insurance adjusters are trained to settle claims quickly and cheaply. They may contact you shortly after the accident with a settlement offer that seems reasonable in the moment but fails to account for future medical costs, long-term disability, or the full value of your pain and suffering. Once you accept a settlement, you typically cannot go back for more money, even if your condition worsens. This is why it is critical to consult a personal injury attorney before accepting any lowball settlement offer.

Types of Injuries Common in Rideshare Accidents

Rideshare accidents can cause a wide range of injuries, from minor soft tissue damage to life-altering conditions. The severity of your injuries directly impacts the value of your claim and the importance of having experienced legal representation. According to one compilation of rideshare accident statistics, 20 to 30 percent of rideshare accidents result in injuries requiring medical attention, with serious injuries — including traumatic brain injuries and spinal cord damage — occurring at a significant rate.

Common injuries in rideshare crashes include:

- Whiplash and soft tissue injuries — often underestimated initially but capable of causing chronic pain and long-term disability

- Traumatic brain injuries (TBIs) — ranging from mild concussions to severe cognitive impairment requiring years of rehabilitation

- Spinal cord injuries — which can result in partial or complete paralysis and permanent changes to quality of life

- Broken bones and fractures — particularly common in high-impact collisions involving multiple vehicles

- Internal organ damage — which may not be immediately apparent and requires prompt medical evaluation to diagnose

- Psychological trauma — including PTSD, anxiety, and depression, which are recognized and compensable injuries under personal injury law

Each of these injury types requires different medical treatment, different specialists, and different approaches to calculating damages. An experienced personal injury attorney understands how to document and present these injuries to maximize your compensation.

What Damages Can You Recover After a Rideshare Crash?

If you were injured in an Uber or Lyft accident, you may be entitled to compensation for a broad range of damages beyond just your immediate medical bills. A comprehensive claim should account for all of the ways the accident has affected your life, both now and in the future.

Economic Damages are those with a specific dollar value:

- Emergency room visits, surgeries, and hospitalization costs

- Ongoing medical treatment, physical therapy, and rehabilitation

- Prescription medications and medical equipment

- Lost wages from time missed at work during recovery

- Diminished earning capacity if your injuries affect your ability to work long-term

- Future medical expenses for long-term or permanent injuries

Non-Economic Damages compensate for the intangible harms caused by the accident:

- Physical pain and suffering, both past and future

- Emotional distress and psychological trauma

- Loss of enjoyment of life and inability to participate in activities you previously enjoyed

- Loss of consortium, meaning the impact of your injuries on your relationships with family members

In cases involving particularly reckless or egregious conduct — such as a driver who was intoxicated or had a known history of dangerous behavior — punitive damages may also be available. These are designed to punish the wrongdoer and deter similar behavior in the future.

Steps to Take Immediately After an Uber or Lyft Accident

The actions you take in the hours and days following a rideshare accident can significantly affect the outcome of your claim. Follow these steps to protect your rights and preserve your ability to recover full compensation.

- Call 911 immediately. Even if injuries seem minor, a police report creates an official record of the accident that is essential for your claim.

- Seek medical attention right away. Do not wait to see a doctor. Delayed treatment can be used by insurance companies to argue that your injuries were not serious or were not caused by the accident.

- Document everything at the scene. Take photos and videos of the vehicles, road conditions, traffic signals, your injuries, and any other relevant details. Photograph the driver’s license, insurance card, and vehicle registration.

- Get witness information. Collect the names and contact information of anyone who saw the accident.

- Report the accident in the rideshare app. Both Uber and Lyft have in-app accident reporting features. This creates a timestamped record with the company.

- Do not give recorded statements to insurance companies. Insurers may ask you to provide a recorded statement shortly after the accident. You are not required to do so, and anything you say can be used to minimize your claim. Consult a lawyer first.

- Contact a personal injury attorney. An experienced rideshare accident lawyer can take over communication with the insurance companies, preserve critical evidence, and build the strongest possible case on your behalf.

Can You Hold Uber or Lyft Directly Liable?

While the independent contractor defense makes direct lawsuits against Uber and Lyft challenging, it is not impossible. There are specific circumstances under which the company itself may be held liable, as detailed in our guide on who is liable when your Uber or Lyft ride ends in injury.

- Negligent hiring or retention: If Uber or Lyft failed to conduct a thorough background check on a driver with a history of DUIs, reckless driving, or other serious offenses, the company may share liability for accidents caused by that driver. This is a key aspect of holding trucking companies accountable, and similar principles apply to rideshare companies.

- App-related malfunctions: If a defect in the rideshare app contributed to the accident — for example, by providing incorrect navigation or causing the driver to be distracted — the company may be liable for that defect.

- Multi-apping distraction: Many rideshare drivers run both the Uber and Lyft apps simultaneously to maximize their income. Toggling between two apps while driving is a form of distracted driving. If this behavior contributed to your accident, digital records from both companies may be subpoenaed to prove it.

Frequently Asked Questions About Rideshare Insurance and Medical Bills

Does Uber or Lyft insurance cover me if I was a pedestrian or cyclist hit by a rideshare driver?

Yes. If the Uber or Lyft driver was on an active trip (Periods 2 or 3) when they struck you, the $1 million liability policy covers third parties — including pedestrians and cyclists — not just passengers.

What if the Uber or Lyft driver was at fault, but their app was only in Period 1?

You would be limited to the lower coverage amounts ($50,000 per person / $100,000 per accident), and only after the driver’s personal insurance denies the claim. This is a significant coverage gap that makes legal representation even more important.

Will filing a claim affect my ability to use Uber or Lyft in the future?

No. Filing a personal injury claim after an accident does not affect your ability to use either platform as a passenger.

How long do I have to file a personal injury claim after a rideshare accident?

The statute of limitations for personal injury claims varies by state. In many states, you have two years from the date of the accident to file a lawsuit. However, it is critical to consult a lawyer as soon as possible, because evidence can disappear quickly and important deadlines may apply earlier than you expect.

What if I don’t have my own auto insurance or health insurance?

If you do not have PIP or health insurance, you can still pursue a claim against the at-fault driver’s insurance or the rideshare company’s policy. A personal injury attorney can help you access treatment through medical liens, which allow you to receive care now and pay the provider from your settlement.

What if Uber or Lyft denies my claim?

If the rideshare company’s insurer denies your claim, you have the right to challenge that decision. An attorney can review the denial, gather additional evidence, and file a lawsuit if necessary. Do not accept a denial as the final word.

Why Pencheff & Fraley Is the Right Choice for Your Rideshare Accident Case

Rideshare accident cases are not like ordinary car accident claims. They require a deep understanding of corporate insurance structures, digital evidence, and the evolving legal landscape surrounding the gig economy. At Pencheff & Fraley, our personal injury attorneys bring that expertise to every case we handle.

We know how insurance companies think, and we know how to counter their tactics. We work on a contingency fee basis, which means you pay nothing unless we win your case. From the moment you contact us, we handle all communication with the insurance companies so you can focus on your recovery.

Our team will:

- Conduct a thorough investigation of your accident, including subpoenaing app data and digital records

- Identify every available source of insurance coverage

- Document the full extent of your injuries and their long-term impact

- Negotiate aggressively for the maximum settlement you deserve

- Take your case to trial if the insurance company refuses to offer fair compensation

Contact Pencheff & Fraley Today — Your Free Consultation Awaits

If you or a loved one has been injured in an Uber or Lyft accident, do not wait. The insurance companies are already building their case. You need an experienced advocate on your side. Contact Pencheff & Fraley today for a free, no-obligation consultation. We will review the details of your accident, explain your legal options, and tell you exactly what your case may be worth, at no cost to you.

Call us today or fill out our online contact form to get started.

Frequently Asked Questions About Rideshare Accidents

What should I do if I’m injured as a passenger in an Uber or Lyft?

If you are injured as a passenger, your first priority is to seek medical attention. Then, document the scene, report the accident in the app, and contact a personal injury lawyer to understand your rights and the complex insurance situation.

What is a catastrophic personal injury claim?

A catastrophic personal injury claim involves injuries that are so severe they result in permanent disability, disfigurement, or a long-term medical condition that fundamentally alters the victim’s life.

How do you prove a traumatic brain injury in court?

Proving a traumatic brain injury (TBI) in court is challenging due to the often “invisible” nature of the injury. It requires extensive medical documentation, expert testimony from neurologists and other specialists, and often neuropsychological testing to objectively demonstrate the cognitive and functional impairments.

What are some common questions about personal injury cases?

Our Personal Injury FAQs page answers many common questions, including how to protect your rights, what a claim is worth, and how contingent fees work.